Why More Inventory Matters More Than a 0.5% Rate Drop | Vancouver WA Real Estate

Why More Inventory Matters More Than a 0.5% Rate Drop for Vancouver WA Buyers

The math is clear — and it's not even close. Here's what rising Clark County inventory actually means for your purchase price, negotiating power, and the real cost of waiting.

Most buyers in Vancouver WA and Clark County are watching mortgage rates like a hawk right now — waiting for a specific number before they commit. That instinct is understandable. But it's costing some buyers real money, and here's what the rate headlines aren't telling you. Whether you're relocating to Vancouver WA from another state or already living in Clark County and ready to move up, the same math applies.

As a Clark County agent who has worked with buyers through both the multiple-offer frenzies of 2022 and the more negotiable market emerging now, I can tell you the difference in real transaction outcomes is not subtle. If you've been wondering whether the Vancouver WA housing market is actually shifting — it is, and the shift favors prepared buyers. The cost of living in Vancouver WA already gives buyers an edge over Portland; rising inventory compounds that advantage significantly. Of the buyer transactions I've closed in Clark County over the past 18 months, a significant and growing share involved sellers accepting below asking price and contributing toward closing costs — a combination essentially unavailable in 2022.

How Much Does a 0.5% Rate Drop Actually Save on a Clark County Home?

Start with the numbers, because they anchor everything that follows.

On a $475,000 home in Clark County with 10% down, your loan amount is roughly $427,500. At a 6.5% rate, your principal and interest payment runs approximately $2,702 per month. (Based on a $427,500 loan amount, 30-year fixed, standard amortization.) Drop that rate by 0.5% to 6.0%, and your payment falls to approximately $2,563 — a difference of about $139 per month. Keep in mind your full monthly cost also includes property taxes in Vancouver WA, which vary by area and are worth factoring into your total payment calculation.

Over three years — a reasonable horizon before many buyers refinance — that rate drop saves roughly $5,184. That's real money. But now compare it to what a rising-inventory market can save you in a single negotiation.

Why Does Rising Inventory Give Buyers More Leverage Than a Rate Drop?

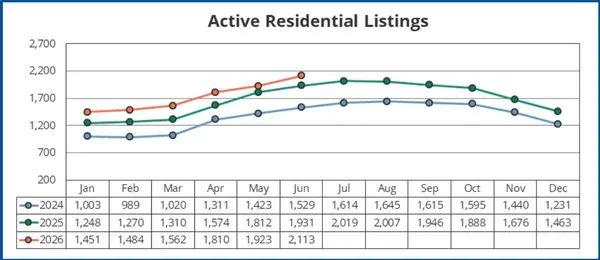

When housing supply is tight, buyers compete. And when buyers compete, prices climb, concessions disappear, and inspection contingencies get waived just to stay in the game. That's the environment Clark County buyers navigated from 2022 through early 2026.

When inventory rises, the math flips entirely. Here's how the same home plays out in both environments — specifically in the $450K–$575K range in Clark County, the tier most sensitive to inventory movement. This includes much of East Vancouver and the Camas corridor:

| Scenario | Purchase Price | Seller Concessions | Contingencies | Net Buyer Position |

|---|---|---|---|---|

|

Low Inventory Multiple offers, 6.5% rate |

$15K–$20K over ask | None accepted | Waived to compete | Buyer absorbs all risk + premium |

|

Rising Inventory 25+ days on market, 7.25% rate |

$8K under ask | $10K toward closing / buydown | Inspection + financing accepted | $25K–$30K total advantage vs. low-inventory scenario |

|

Rate Drop Only 6.0% rate (waited 8 months) |

Prices up 4%+ during wait | Competition returned with rate drop | Market tightened again | Rate savings erased by price appreciation |

What Is the Lock-In Effect and How Does It Affect Clark County Housing Supply?

To understand why inventory is rising now — and why that matters — you need to understand why it was so compressed in the first place.

During the pandemic, millions of homeowners locked in mortgage rates between 2.5% and 3.5%. Moving today means trading that rate for something in the 6.5%–7.25% range. On a $400,000 loan, that difference represents $700–$900 more per month. For most homeowners, that math doesn't work unless life forces the issue.

According to Federal Housing Finance Agency research, this lock-in effect has been the primary structural force constraining housing supply since mid-2022. It's not a traditional shortage — it's a behavioral freeze caused by rate spreads that make moving financially irrational for many existing homeowners. This dynamic affects Portland vs. Vancouver differently too — Clark County's lower tax burden means the financial case for staying put is slightly less extreme here than across the river, which is part of why inventory is starting to move.

How Does New Construction Inventory in Clark County Affect Buyers Right Now?

The rising inventory story in Clark County isn't only about existing homes. The new construction corridors in Ridgefield, Battle Ground, and Camas / La Center have added meaningful supply, and builders are competing aggressively for buyers. If you're weighing existing homes vs. new builds, see the full breakdown of the best new construction neighborhoods in Vancouver WA for 2026 and the complete guide to buying new construction in Vancouver WA.

According to NAR data, new construction now makes up over 31% of all homes for sale nationally — compared to a historical average (pre-2020) closer to 13%. That shift is visible across Clark County's northern growth corridors, where spec inventory has accumulated as buyer absorption has slowed.

A buyer looking at a $500,000 new build in Ridgefield today can often negotiate a 2-1 rate buydown funded entirely by the builder — lowering their effective first-year rate by 2% and second-year rate by 1%, with no out-of-pocket cost. That tool exists specifically because inventory is up and builders need to move product. It is not available in a tight market. Here's a deeper look at why new construction works so well for buyers right now — and if you're going the builder route, make sure you read how to protect yourself from bad builders before you sign anything. Also worth comparing: Ridgefield vs. Camas — two of Clark County's most active new construction markets with very different community feels.

Should First-Time Buyers in Vancouver WA Wait for Lower Rates or Buy Now?

The rate obsession is understandable — you have no equity to roll, every dollar of payment matters. But waiting has a real cost: according to the Federal Housing Finance Agency House Price Index, Washington state home prices rose 4.2% year-over-year as of Q4 2025. On a $450,000 home, that's $18,900 in additional purchase price after just 12 months of waiting. Add rent paid during that period, and the gap between "waiting for a better rate" and "buying when inventory supports you" widens considerably.

The practical move: Get pre-approved, identify homes with 21+ days on market in your target zip code — areas like Salmon Creek, The Orchards, and Minnehaha consistently offer strong first-time buyer value. For a full picture of where your budget goes furthest, see the guide to the most affordable neighborhoods in Vancouver WA. Then negotiate a seller-paid 2-1 buydown. That lowers your effective rate by 2% in year one — more payment relief than a 0.5% permanent rate drop, available today.

If you already own a Clark County home and have been sitting on equity, the case for acting is arguably stronger. Your down payment source doesn't care what the Fed does — it's the equity in your current home. What it does care about is how long you wait while appreciation continues on the home you want to buy next.

A practical example: A move-up buyer targeting a $650,000 Camas home with $150,000 in equity from a current Vancouver property can realistically negotiate $635,000, request $12,000 in seller concessions toward a buydown, and still land a manageable payment — with a clear refinance path when rates normalize. Downsizing instead? The top neighborhoods for retirees in SW Washington are seeing the same inventory-driven flexibility. Waiting for a 0.5% rate improvement adds roughly $60/month in savings. Losing the negotiating window because rates drop and 200 sidelined buyers re-enter the market costs far more.

Why Do Lower Mortgage Rates Sometimes Coincide With Worse Buying Conditions?

This is the piece of the rate-waiting argument that rarely gets discussed — and it matters most for buyers on Clark County's $400K–$575K tier.

Mortgage rates don't fall in a vacuum. When rates drop significantly, it's typically because the broader economy is slowing. A slowing economy brings job uncertainty, tighter lending standards, and lower consumer confidence. The buyers who spent 12 months waiting for rates to fall often find themselves hesitating anyway — because the same conditions that produced lower rates also produced anxiety about large financial commitments.

How to Use a Rising-Inventory Market in Clark County Today

Whether you're buying your first home or your third, here's what this means in practice — steps you can take this week.

What Vancouver WA Buyers Are Asking Right Now

Why does inventory matter more than interest rates for home buyers?

Inventory determines negotiating leverage. A 0.5% rate drop saves roughly $130–$145 per month on a typical Clark County purchase — about $5,000 over three years. But buying in a higher-inventory market can mean $15,000–$25,000 less in purchase price plus seller concessions that reduce upfront costs. The compounded savings from favorable market conditions can exceed years of rate-drop benefit in a single transaction.

How much does a 0.5% rate drop save on a $450,000 home in Washington state?

On a $450,000 purchase with 10% down ($405,000 loan, 30-year fixed), a 0.5% rate drop saves approximately $135–$140 per month in principal and interest. Over 36 months, that totals roughly $4,700–$5,000 — less than the value of one well-negotiated seller concession in today's Clark County market.

What is a buyer's market in Clark County WA real estate?

A buyer's market in Clark County occurs when active listings exceed roughly 3–3.5 months of supply, giving buyers the ability to negotiate on price, include contingencies, request repairs, and ask for closing cost contributions. When homes average 21-plus days on market and list-to-sale ratios fall below 99%, buyers are operating with leverage that didn't exist from 2022 through mid-2025.

Can a seller pay for a mortgage rate buydown in Washington state?

Yes. Washington state sellers can contribute toward a buyer's closing costs, which can include a temporary or permanent mortgage rate buydown. A 2-1 buydown funded by the seller lowers the buyer's rate by 2% in year one and 1% in year two, meaningfully reducing early monthly payments. This concession is most negotiable in higher-inventory markets — like Clark County's current environment — where sellers need to differentiate their listing.

Is now a good time to buy a house in Vancouver WA?

For financially prepared buyers, rising inventory in Clark County is creating conditions not widely available since before 2022: motivated sellers, negotiable prices, and accessible seller concessions including rate buydowns. While mortgage rates remain elevated compared to 2020–2021 levels, the combination of more supply, moderating price growth, and available buydown tools means the total cost of buying now may be lower than waiting for a rate target that may arrive alongside higher prices and renewed competition.

Ready to Stop Waiting and Start Negotiating?

The inventory window in Clark County is open right now. As a local agent who tracks list-to-sale ratios, days on market, and builder incentives across Vancouver WA weekly — I can show you exactly where the leverage is in your price range and target neighborhood. Let's talk.

Schedule a Free Discovery Call Get the Free SW WA Relocation GuideCategories

Recent Posts

GET MORE INFORMATION

Cassandra Marks

Realtor, Licensed in OR & WA | License ID: 201225764

Realtor, Licensed in OR & WA License ID: 201225764