Mortgage Rates 2026: Buy Now or Wait in Clark County WA?

Should You Buy Now or Wait? Clark County Mortgage Rates in 2026

Rates didn't drop to 6% like everyone predicted. Here's what actually happened — and what it means for buyers in Clark County right now.

I want to be straight with you about something. At the start of 2026, a lot of buyers were told to wait — that mortgage rates were expected to drop below 6%, potentially even into the mid–5% range, and that patience would be rewarded as the market loosened up. We even saw a brief dip near 5.99%, which gave that expectation a short-lived reality. But that window didn’t hold. Rates moved back up and have since stabilized around 6.5%, and the broader “lower-rate” scenario hasn’t played out the way many forecasts suggested.

Today, May 4th, rates are sitting at roughly 6.5%. NAR's Chief Economist Lawrence Yun — who predicted 14% sales growth for 2026 — has already walked that back to 4%. The market didn't do what anyone expected. What it did do, though, is give buyers something they haven't had in years: options and leverage. And that changes the calculus for buyers who are sitting on the fence right now.

Here's a clear-eyed look at where things actually stand today — and what it means if you're thinking about buying in Clark County, Washington.

- Mortgage rates are hovering around ~6.5% after briefly dipping near 5.99% earlier in 2026

- Expectations for rates moved from below 6% (mid–5% range) back up as the market reversed course

- NAR's Lawrence Yun revised 2026 sales growth from 14% down to 4% — a significant reset of expectations

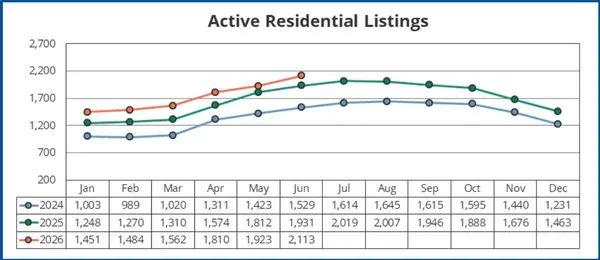

- Housing inventory is up 25% year-over-year — buyers have more choices and more leverage than in years

- Buyers can now negotiate price reductions, seller credits, and rate buydowns — concessions that weren't available in 2021–2023

- Waiting for 5% rates means competing with a flood of buyers who were also waiting — likely in a market with less inventory and higher prices

What Lawrence Yun's Revised Forecast Actually Tells Us

NAR Chief Economist Lawrence Yun entered 2026 forecasting 14% growth in existing home sales. That was an optimistic picture — built on an assumption that rates would fall meaningfully and pent-up buyer demand would unleash. Then the Fed stayed cautious, rates stayed elevated, and Yun revised the forecast down to approximately 4% growth.

What does a downward revision from 14% to 4% actually mean for buyers? Less competition than originally anticipated. Fewer bidding wars. Sellers who have had to recalibrate their expectations. A market that — quietly and without a lot of fanfare — has shifted a meaningful degree in the buyer's direction.

Why Rates Are Flat at 6.5% — and What to Expect

The prediction was that rates would drift toward 6% by mid-2026. The reality is they're holding at roughly 6.5%. The Federal Reserve has been cautious — prioritizing inflation control over rate relief — and that caution has kept mortgage rates elevated longer than most forecasters expected.

Here's the honest answer on where rates go from here: nobody actually knows. The forecasters who were confident about 6% were wrong by half a point. That half-point matters on a mortgage. What we can say with more confidence is that rates at some point will come down — and when they do, every buyer who is sitting in a home will have the option to refinance. Every buyer who was waiting will suddenly be competing again.

| Scenario | Rate | Monthly Payment (on $500K loan) | Difference from Today |

|---|---|---|---|

| Today (May 2026) | 6.5% | ~$3,160/mo | — |

| If rates drop to 6.0% | 6.0% | ~$2,998/mo | -$162/mo |

| If rates drop to 5.5% | 5.5% | ~$2,839/mo | -$321/mo |

| If you wait + prices rise 5% | 6.0% | ~$3,148/mo | -$12/mo net savings |

The Inventory Edge: More Homes, More Options, More Leverage

This is the part of the 2026 market that isn't getting enough attention. While everyone is focused on rates, inventory has quietly shifted significantly in buyers' favor. Year-over-year, housing inventory is up approximately 25%. That number deserves a moment to sink in.

In 2021 and 2022, buyers were writing offers on homes they'd seen once, waiving inspections, offering tens of thousands over asking price, and losing anyway. That market is gone. The current market in Clark County has homes sitting longer, sellers making concessions, and buyers with the ability to actually think before they act.

Why Waiting for 5% Might Be a Mistake

The idea of waiting until rates hit 5% is psychologically appealing. It feels disciplined. But here's what waiting for 5% actually looks like in practice.

The moment rates drop significantly, every buyer who was waiting does exactly the same thing: they re-enter the market simultaneously. Demand surges. Inventory gets absorbed fast. Sellers who were making concessions stop making them. Prices move. And the buyer who was "being patient" finds themselves in a more competitive market, paying more for less house, with less room to negotiate.

The buyers who win when rates drop aren't the ones who waited for them — they're the ones who already own a home and refinance into the lower rate.

- 25% more inventory to choose from

- Real negotiating power on price and terms

- Sellers offering credits and buydowns

- Time to do proper due diligence

- Lock in today's home price

- Refinance when rates eventually drop

- Start building equity now

- More buyers re-enter simultaneously when rates drop

- Inventory gets absorbed — fewer choices

- Sellers stop making concessions

- Home prices likely rise with demand

- Bidding wars return in popular neighborhoods

- You lose months or years of equity building

- Net monthly savings may be minimal after price increases

How to Use Today's Market to Negotiate Hard

With more homes available and fewer buyers competing for each one, the negotiating dynamics have shifted. Here's what you can realistically ask for in the current Clark County market — and what actually tends to move.

Mortgage Rates & Buying in 2026: Common Questions

Should I buy a home now or wait for lower mortgage rates in 2026?

Based on current data as of May 2026, buying now makes more strategic sense for most Clark County buyers than waiting. Mortgage rates are flat at approximately 6.5% — not dropping toward 6% as forecast. Meanwhile, inventory is up 25% and negotiating leverage is the strongest it has been since before 2021. The strategic play is to buy now at favorable inventory conditions, negotiate hard, and refinance when rates eventually fall. Waiting means re-entering a market alongside every other buyer who was also waiting — likely with less inventory, higher prices, and fewer concessions available.

What are mortgage rates doing in 2026?

As of May 4, 2026, 30-year fixed mortgage rates are holding at approximately 6.5%. This is higher than the 6% level that NAR's Lawrence Yun originally forecast for 2026. The Federal Reserve's cautious approach to rate cuts has kept rates elevated relative to early-year expectations. Most forecasters still expect rates to gradually decline over the medium term, but the timeline is uncertain.

What did NAR revise in its 2026 housing forecast?

NAR Chief Economist Lawrence Yun revised the 2026 existing home sales growth forecast from approximately 14% down to approximately 4%. The revision reflects persistent mortgage rates staying higher than expected and more cautious buyer activity than originally projected. Despite the downward revision in sales volume, housing inventory has increased approximately 25% year-over-year, which is a positive development for buyers in terms of choice and negotiating power.

What does 'marry the house, date the rate' mean?

"Marry the house, date the rate" is a home buying strategy that means committing long-term to the right property at today's price, while treating the mortgage rate as temporary. When rates eventually fall, you refinance to a lower rate. The logic: you control when you refinance, but you cannot go back and purchase a home at a lower price after values have risen. Locking in your home purchase now while inventory is elevated and negotiating leverage is strong, then refinancing when rates improve, is the core of this strategy.

Popular term that many realtors threw around but you need to plan for that interest rate to stay right where it is for the foreseeable future. Do not plan on a reduction in rate for a refi. So it is important to be comfortable with your payment right now.

Is the Clark County WA housing market good for buyers in 2026?

Yes — Clark County's 2026 market is more buyer-friendly than it has been since before 2021. Inventory is up approximately 25% year-over-year. Days on market in Vancouver WA average 76 days. Sellers are more open to price reductions, seller credits, rate buydowns, and flexible timelines than during the ultra-competitive 2021–2023 period. Combined with Washington state's tax advantages for buyers relocating from Oregon — no state income tax on WA wages, lower property tax rates — Clark County represents strong overall value in the Pacific Northwest market.

Ready to See What's Available in Clark County Right Now?

Inventory is up 25%. Negotiating leverage is real. If you've been sitting on the fence, now is the time to see what your budget actually gets you — before the rate drop brings every waiting buyer back to the table.

Browse Clark County Listings Talk to Cassandra

Categories

Recent Posts

GET MORE INFORMATION

Cassandra Marks

Realtor, Licensed in OR & WA | License ID: 201225764

Realtor, Licensed in OR & WA License ID: 201225764