First-Time Home Buyer in Vancouver, WA? Here’s What You Really Need to Know

First-Time Home Buyer in Vancouver, WA? Here’s What You Really Need to Know

Understanding the Vancouver Real Estate Market

by Cano Real Estate

by Cano Real Estate

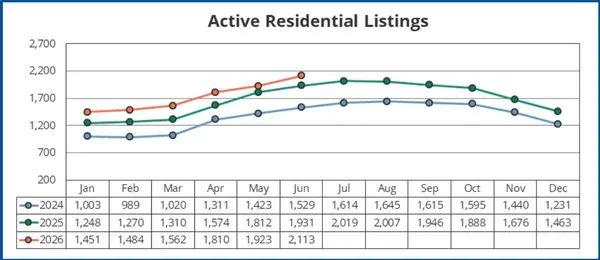

Current Market Snapshot: Vancouver, WA Housing Trends in 2025

If you're a first-time home buyer in Vancouver, WA, you're stepping into one of the Pacific Northwest's most dynamic and fast-growing housing markets. As of April 2025, the Vancouver, Washington real estate market continues to show steady growth. The median home price in Vancouver is approximately $510,138, marking a 2.3% increase compared to the previous year. This consistent upward trend reflects strong demand and a competitive housing landscape, particularly for entry-level homes.

Homes in Vancouver are selling quickly—typically within 40 days or less on the market—and many are attracting multiple offers, especially in sought-after neighborhoods near downtown, popular school zones, and with easy access to I-5 and SR-14. These market conditions mean that timing, preparation, and professional guidance are more critical than ever for buyers looking to secure the right home without overpaying.

Why Vancouver Appeals to First-Time Home Buyers

So why are so many people—especially first-time home buyers—choosing to plant roots in Vancouver, Washington? It comes down to a unique combination of affordability, location, lifestyle, and tax advantages that few cities in the region can match.

1. Strategic Location Without the High Price Tag

Vancouver sits just across the Columbia River from Portland, Oregon. This gives residents easy access to Portland’s job market, nightlife, and airport—without the Oregon income tax. That’s right: Washington has no state income tax, which can save homeowners thousands of dollars a year. Many first-time buyers working in Portland choose to live in Vancouver for the financial advantage and small-town charm.

2. Affordable Neighborhoods With Big Value

Compared to Portland, Seattle, or even Beaverton, Vancouver offers more house for the money. Neighborhoods like Hazel Dell, Orchards, and Salmon Creek are popular with first-time buyers due to their affordable home prices, access to schools, and proximity to shopping, parks, and employers. For those looking for a starter home or a townhouse with space to grow, these communities offer ideal starting points.

Some emerging neighborhoods and suburban areas like East Minnehaha, Five Corners, and Walnut Grove are also gaining traction with first-time buyers looking for a combination of value and convenience.

3. Quality of Life and Outdoor Lifestyle

Vancouver is renowned for its access to the outdoors—something that’s especially appealing to Millennial and Gen Z homebuyers. With more than 90 parks, scenic hiking trails, and the Columbia River waterfront nearby, it’s easy to live an active lifestyle without leaving the city. Popular nearby attractions like Waterfront Park, Fort Vancouver, and Frenchman’s Bar provide weekend getaways without the long drive.

Plus, the city offers an ever-growing number of locally-owned coffee shops, breweries, dog parks, and farmers markets—giving Vancouver a vibrant community vibe that first-time buyers are drawn to.

4. Strong Local Schools and Family-Friendly Appeal

For buyers planning to start or grow a family, Vancouver’s public school systems, including Vancouver Public Schools and Evergreen Public Schools, are well-regarded in the region. The area is also home to a number of charter and magnet schools, making it an excellent place to put down roots and plan for the future.

5. Investment Potential for First-Time Buyers

Vancouver has proven to be a smart long-term investment for homeowners. Home values have steadily appreciated over the past decade, and the city’s continued population growth and development (especially around the Vancouver Waterfront and downtown) point to ongoing value for those entering the market now. First-time buyers often find themselves in a stronger equity position just a few years after purchasing, especially in up-and-coming areas.

What First-Time Home Buyers Need to Know

by Go With Ro Vancouver, WA Real Estate

by Go With Ro Vancouver, WA Real Estate

From financing options to home tours—here’s what to expect when buying your first home in Vancouver, WA

The Truth: It’s Normal to Feel Overwhelmed at First

Let’s be honest—buying your first home can feel a little like jumping into the deep end. Mortgage terms, credit scores, home inspections, earnest money... what does it all mean?

If you're a first-time home buyer in Vancouver, WA, know this: you’re not alone, and you don’t have to figure it all out by yourself. That’s exactly why I (Cassandra Marks—aka “Realtor Cas”) team up with amazing lenders like Heather Vezzetti to host our live, in-person events like “What You Need to Know: Buying Your First Home” at Heathen Brewing Feral Public House.

These sessions are designed to remove the confusion, answer your questions, and give you a realistic game plan to go from curious to confident.

Step 1: Know What You Can Afford

One of the first steps to buying a home is understanding your budget—and no, you don’t need to have it all figured out ahead of time.

Your lender (like Heather) will work with you to determine:

-

Your pre-approval amount

-

What kind of monthly mortgage payment fits your lifestyle

-

Whether you qualify for down payment assistance programs in Washington

-

What your debt-to-income ratio looks like

-

How much you'll need for closing costs, reserves, and inspections

Step 2: Get Pre-Approved (Not Just Pre-Qualified)

In a competitive market like Vancouver, being pre-approved (with underwriting review) gives you a huge edge. Sellers want to know you’re serious—and it can make your offer more attractive.

During our classes, Heather breaks this all down with zero sales pitch and all straight talk. You’ll walk away understanding what pre-approval means, how long it lasts, and what to do if your credit isn’t quite ready yet.

Step 3: Buyer Strategy Session—Tailored to YOU

After class, most of our attendees set up a 1-on-1 Buyer Strategy Session with me. Here’s what we’ll talk about:

-

Your ideal timeline (Ready now? 6 months out? Just dreaming? All good!)

-

What kind of home and neighborhood fit your goals

-

How to search smart using MLS tools (no, Zillow doesn’t show everything)

-

How to compete in multiple-offer scenarios

-

What’s going on in your specific price range in Vancouver, Hazel Dell, or wherever you’re looking

Step 4: Touring Homes and Making Offers

Once you’re pre-approved and your game plan is in place, it’s time to start the fun part—touring homes!

Here’s what first-time buyers in Vancouver need to know:

-

Many homes sell quickly (within a few days), so seeing a house right away matters.

-

I’ll help you read between the lines: What’s up with that foundation? What does “as-is” really mean? Is that roof newer or 25 years old?

-

We’ll break down what happens once you’re ready to make an offer: contingencies, earnest money, inspections, and timelines.

Step 5: Inspections, Appraisals, and Closing

After your offer is accepted, the real work begins—don’t worry, I’ll walk you through every step. Here's what typically happens in Vancouver-area purchases:

-

Inspection period: 5–10 days to have a licensed inspector evaluate the home

-

Appraisal: Your lender ensures the home is worth the purchase price

-

Loan underwriting: Final review of your documents

-

Closing: Sign your papers (in person or virtually) and receive your keys!

Frequently Asked Questions From Our Live Events

Do I need perfect credit to buy a home?

Not at all. There are loan programs for buyers with credit scores as low as 580, though higher scores open up more options. We’ll walk you through how to build credit and prepare your finances if you’re not quite ready.

Can I buy a home if I’m self-employed?

Absolutely—it just takes more documentation. We’ll show you how to prep your tax returns, P&L statements, and other details lenders want to see.

Is it okay if I’m not ready to buy right away?

YES! Our goal is to educate and empower—not pressure. Many people take the class a year before they buy. Starting early sets you up for success when the time is right.

What if I want to buy with a friend or family member?

That’s becoming more common, especially for first-time buyers looking to split costs or co-invest. We’ll talk through the legal and financial considerations of shared ownership.

Why Education and Community Matter

Buying a home isn’t just a transaction—it’s a life transition. That’s why we hold these free, all-ages events in fun, no-pressure settings like breweries and coffee shops. We want to make this process approachable and real.

There’s no sales pitch, just practical advice from a team who’s helped hundreds of Vancouver first-time buyers become confident homeowners.

And yes—we always have light appetizers, pizza, and plenty of Q&A. Come curious, come hungry (literally), and bring your questions!

Financing 101 – Breaking Down Loans, Grants, and Assistance Programs

How to finance your first home in Vancouver, WA without draining your savings

Let’s Talk Money—Without the Intimidation

Financing is often the #1 thing that holds people back from becoming homeowners. Maybe you've heard myths like “You need 20% down” or “Your credit score has to be perfect.” Let's bust those myths right now.

Whether you're fresh out of school, self-employed, or just tired of paying rent, this chapter breaks down exactly how first-time home buyers in Vancouver, WA can finance their home purchase—without panic, and possibly without a big down payment at all.

The Most Common Loan Types for First-Time Buyers

In partnership with local lenders like Heather Vezzetti, we help buyers understand their best loan options. Here’s what’s most common in Southwest Washington:

1. FHA Loans

-

Best for: Buyers with lower credit scores (580+) or limited down payments

-

Minimum down payment: 3.5%

-

Benefits: Flexible credit requirements, low rates

-

Considerations: Mortgage insurance required for the life of the loan

2. Conventional Loans

-

Best for: Buyers with good credit (620+) and some savings

-

Minimum down payment: 3% (for first-time buyers!)

-

Benefits: More flexible property types, private mortgage insurance (PMI) can be removed once you hit 20% equity

-

Considerations: Tighter qualification standards than FHA

3. VA Loans

-

Best for: Veterans, active-duty service members, eligible spouses

-

Minimum down payment: 0%

-

Benefits: No PMI, competitive interest rates, low closing costs

-

Considerations: Only available to those with VA eligibility

4. USDA Loans

-

Best for: Buyers in eligible rural/suburban areas (yes, some areas near Vancouver qualify!)

-

Minimum down payment: 0%

-

Benefits: No PMI, low interest rates

-

Considerations: Income and location restrictions

Washington State First-Time Buyer Assistance Programs

Washington is one of the most supportive states for first-time home buyers, offering several programs through the Washington State Housing Finance Commission (WSHFC).

Home Advantage Program

-

Offers below-market interest rates on FHA, VA, USDA, or conventional loans

-

Must complete a WSHFC-approved buyer education course (online or in-person)

Home Advantage Downpayment Assistance

-

Offers up to 4% of the loan amount as a second mortgage—deferred payment, 0% interest

-

Must pair with a WSHFC loan product

House Key Opportunity Program

-

Similar to Home Advantage but for lower-income borrowers

-

Income and purchase price limits apply

Local Clark County Assistance Programs

In addition to state programs, first-time buyers in Clark County or the City of Vancouver may qualify for:

-

City of Vancouver Homeownership Assistance Program (via local nonprofits or housing organizations)

-

Community Development Block Grants (CDBG) for down payments or closing costs

-

Employer-based programs, especially for healthcare or education workers

Heather and I stay up-to-date on these offerings and can help you apply for assistance you may not even know you qualify for.

Getting Pre-Approved: Step-by-Step

Pre-approval is your golden ticket in today’s market. Here’s what you’ll typically need:

-

Last two years of W-2s or tax returns

-

Pay stubs from the last 30 days

-

Bank statements (2 months)

-

Credit check authorization

-

Photo ID

You’ll get a pre-approval letter showing how much you can afford—and we’ll help you shop smart based on your monthly budget, not just your max price.

Buyer Tip: Don’t Open New Credit Cards or Finance a Car

Once you’re pre-approved, hold off on any major purchases or new credit accounts until after closing. Changes in your credit profile can affect your loan approval!

Closing Costs 101

Beyond your down payment, expect to pay 2–5% of the purchase price in closing costs. These may include:

-

Appraisal fees

-

Title insurance

-

Lender fees

-

Escrow setup (taxes and homeowners insurance)

🎯 Did you know sellers in Vancouver often agree to cover some or all closing costs for first-time buyers? We’ll negotiate hard for that on your behalf.

What If You’re Not Ready Today?

No worries—many buyers start the planning process 6–12 months in advance. We’ll help you:

-

Build or repair credit

-

Start saving for a down payment

-

Pay off key debts

-

Map out your future purchase timeline

Education is the most powerful tool for first-time buyers. That’s why Heather and I offer our free “What You Need to Know” home buyer workshops—because when you understand your finances, you’re in control.

Touring Homes in Vancouver – What to Expect and How to Know It’s the One

by Redfin

by Redfin

The real-life experience of house hunting with Realtor Cas—what first-time buyers should know before stepping through the front door.

You’ve Got the Pre-Approval… Now What?

This is where things start to feel real. You’ve done your research. Your financing is lined up. And now it’s time to actually see homes in person.

But don’t worry—you’re not doing it alone.

When I tour homes with first-time buyers, I like to say: “This is the fun part—but we’re also gathering data.” It’s a mix of emotion and strategy. You’ll feel excited, a little overwhelmed, and maybe surprised by what you love (or don’t).

Vancouver’s Neighborhoods – Where First-Time Buyers Look First

Not all homes—and not all neighborhoods—are created equal. Some of the top areas I tour with first-time buyers include:

Hazel Dell

-

Affordable ranch-style homes and condos

-

Close to freeways, shopping, and services

-

Popular with young professionals and small families

Orchards

-

Fast-growing area with newer builds and townhomes

-

Great parks and trails

-

Near high-performing schools and local markets

Minnehaha

-

Quieter, residential vibe with a mix of older homes and updated remodels

-

Centrally located for commuting or weekend escapes

Fourth Plain Village & Rose Village

-

Up-and-coming neighborhoods with lower entry prices

-

Great investment potential and community development projects underway

Open Houses vs Private Tours: What’s the Difference?

You can browse Zillow all day, but nothing replaces being inside a home. Here’s what to expect from two common types of home viewings:

Open Houses

-

Usually held weekends, 1–4 PM

-

No appointment necessary—just walk in

-

Great for casually checking out layout, finishes, and neighborhood vibe

💡 Tip: I always tell buyers to take notes and photos. Homes start blending together fast!

Private Tours with Me (Cassandra)

-

We book a dedicated time just for you

-

No pressure, no distractions

-

I’ll walk you through key details like roof age, furnace systems, signs of DIY work vs. professional upgrades

-

I also watch your body language: if you light up in a kitchen or hesitate in a backyard, I take notes

Questions You Should Be Asking on Every Tour

-

How old is the roof, water heater, and HVAC?

-

How much are the average utility bills?

-

What are the neighbors like?

-

Is the HOA involved—and how strict are they?

-

Is anything on the seller’s disclosure we should be worried about?

I’ll help you read between the lines of flashy staging and smart listing photos. You’re not just buying a home—you’re investing in peace of mind.

How Do You Know It’s "The One"?

Sometimes buyers walk into a home and just know. More often, it takes a little time. Here’s how I help my clients stay grounded:

-

Emotional scorecard: Does the home feel safe, functional, and inspiring?

-

Logic check: Does it align with your budget, commute, lifestyle, and future plans?

-

Resale value: Would this be a smart investment even if it's not your forever home?

Remember: your first home doesn’t have to be your dream home—but it should set you up for the next chapter in your life.

Common Mistakes First-Time Buyers Make While Touring Homes

-

Falling for decor and ignoring structure.

Pretty staging doesn’t mean the electrical is up to code. -

Skipping the inspection.

Never. Ever. Skip. The. Inspection. -

Ignoring the commute.

That cute place 45 minutes away? It gets old real fast when it’s raining in February. -

Overlooking the neighborhood at different times of day.

Drive by at night or during rush hour. Talk to neighbors. Check noise levels.

The "It Just Feels Right" Factor

Listen, this is your home. Not your investor’s. Not your parents’. Not your friends’ idea of what you should buy. If it feels like a place where you can breathe, laugh, rest, and build—that matters.

And when the house is right, we’ll move fast. Vancouver’s market is still competitive in 2025, especially under $550K. That’s why I always prep buyers with a decision-making checklist and sample offer documents before we go house hunting.

So when you fall in love? You’ll be ready.

Final Thoughts: Your First Home Starts With One Step

Buying your first home in Vancouver, WA, is absolutely within reach. With the right information, the right team, and the right mindset—you can go from “just browsing” to closing on a home you love. This article (and free home buyer class) are designed to help you do just that. So take the first step. Reach out. Ask questions. Show up to the next class. I and Heather will meet you where you are—and guide you the rest of the way home.

Sign up for my monthly newsletter to receive expert advice, important local updates, and insider knowledge on the best ways to thrive in this unique region. Whether you're buying, selling, or simply curious about life in the Pacific Northwest, I've got you covered.

👉 Join my newsletter today and never miss a beat! Just enter your email below and get exclusive access to all things Southwest Washington. Let’s stay connected!

Frequently Asked Questions

How do I qualify as a first-time homebuyer in Washington?

You must not have owned and lived in a primary residence within the last three years, unless qualifying under specific exceptions. You’ll need to complete a homebuyer education course and meet income and purchase price limits. A minimum credit score—usually at least 620—is also required for most programs.

What is the $10,000 grant in Washington state for homeowners?

Washington offers a $10,000 deferred down payment assistance loan through its Home Advantage Needs-Based program. It carries a low 1% interest rate and doesn’t need to be repaid until you sell, refinance, or pay off your home. The program is income-based and meant to help lower-income buyers.

What do most first-time homebuyers get approved for?

Many first-time buyers qualify for down payment assistance ranging from $10,000 to $15,000 through state programs. These funds are typically used for closing costs or reducing the loan amount. Approval amounts depend on income, credit, and loan type.

Is Clark County’s $60,000 in down payment help available to qualifying homebuyers?

Yes, Clark County offers up to $60,000 in down payment and closing cost assistance for eligible buyers. The loan has a 2% simple interest rate and is deferred until resale or refinance. Buyers must meet income and credit requirements and purchase a home under $600,000.

What is the first-time buyer grant in WA?

Washington’s most common first-time buyer support is the Home Advantage Program, which includes down payment loans of up to 5% of the home’s purchase price. It also offers a needs-based $10,000 assistance option for lower-income households. These funds are repaid only when the home is sold or refinanced.

What is the minimum income to qualify for first-time home buyers?

Income limits vary by county and program but generally cap around $180,000 for Washington State Housing Finance Commission programs. Some assistance programs have lower income thresholds, closer to $105,000 depending on household size. Your income must be enough to qualify for the mortgage, even if you meet grant requirements.

What credit score do you need to buy a house in Washington?

Most first-time buyer programs require a minimum credit score of 620. Some programs or lenders may prefer 640 or higher for better terms. FHA and VA loans may allow lower scores but come with stricter financial guidelines.

What is the minimum credit for a first-time homebuyer?

The minimum credit score for most Washington-based programs is 620. FHA loans can go as low as 580 with 3.5% down, or even 500 with a larger down payment. However, higher scores offer more options and better interest rates.

Is the government giving out $10,000 grants?

Washington State provides down payment assistance loans that are often referred to as “grants” but must be repaid eventually. The $10,000 Home Advantage Needs-Based loan is one example, available to income-qualified buyers. It’s a helpful resource for those who can’t afford large upfront costs.

What is the Washington Home Advantage Program?

The Home Advantage Program offers down payment assistance combined with a 30-year fixed mortgage at competitive rates. Buyers can get up to 5% of the loan amount in deferred assistance. It’s open to first-time and repeat buyers who meet income and credit score requirements and complete homebuyer education.

Categories

Recent Posts

GET MORE INFORMATION

Cassandra Marks

Realtor, Licensed in OR & WA | License ID: 201225764

Realtor, Licensed in OR & WA License ID: 201225764